This tale firstly gave the impression on Zacks

If you’re on the lookout for a inventory that has a forged historical past of thrashing profits estimates and is in a just right place to deal with the fad in its subsequent quarterly document, you must believe ResMed (RMD). This corporate, which is within the Zacks Clinical – Merchandise trade, displays doable for any other profits beat.

– Zacks

– Zacks

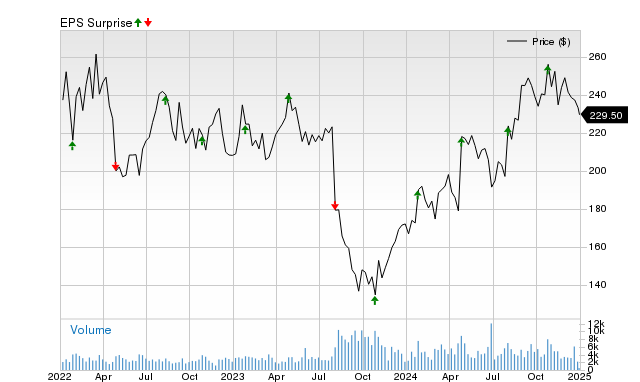

This maker of clinical merchandise for respiration problems has observed a pleasing streak of thrashing profits estimates, particularly when having a look on the earlier two stories. The typical marvel for the ultimate two quarters was once 9.93%.

For the latest quarter, ResMed was once anticipated to submit profits of $1.35 in keeping with proportion, nevertheless it reported $1.51 in keeping with proportion as an alternative, representing a marvel of eleven.85%. For the former quarter, the consensus estimate was once $1.25 in keeping with proportion, whilst it in reality produced $1.35 in keeping with proportion, a marvel of 8%.

Worth and EPS Marvel

With this profits historical past in thoughts, contemporary estimates had been transferring upper for ResMed. In truth, the Zacks Profits ESP (Anticipated Marvel Prediction) for the corporate is sure, which is a brilliant signal of an profits beat, particularly whilst you mix this metric with its great Zacks Rank.

Our analysis displays that shares with the combo of a good Profits ESP and a Zacks Rank #3 (Grasp) or higher produce a good marvel just about 70% of the time. In different phrases, when you’ve got 10 shares with this mixture, the selection of shares that beat the consensus estimate may well be as top as seven.

The Zacks Profits ESP compares the Maximum Correct Estimate to the Zacks Consensus Estimate for the quarter; the Maximum Correct Estimate is a model of the Zacks Consensus whose definition is expounded to switch. The theory here’s that analysts revising their estimates proper ahead of an profits liberate have the newest knowledge, which might probably be extra correct than what they and others contributing to the consensus had predicted previous.

ResMed has an Profits ESP of +1.59% at the present time, suggesting that analysts have grown bullish on its near-term profits doable. While you mix this sure Profits ESP with the inventory’s Zacks Rank #2 (Purchase), it displays that any other beat is perhaps across the nook.

Traders must notice, then again, {that a} unfavourable Profits ESP studying isn’t indicative of an profits omit, however a unfavourable worth does cut back the predictive energy of this metric.

Many corporations finally end up beating the consensus EPS estimate, however that will not be the only real foundation for his or her shares transferring upper. However, some shares would possibly cling their floor even though they finally end up lacking the consensus estimate.

As a result of this, it is in reality vital to test an organization’s Profits ESP forward of its quarterly liberate to extend the percentages of good fortune. You should definitely make the most of our Profits ESP Filter out to discover the most productive shares to shop for or promote ahead of they have reported.

Zacks Best 10 Shares for 2022

Along with the funding concepts mentioned above, do you want to learn about our 10 best alternatives for the whole lot of 2022?

From inception in 2012 via November, the Zacks Best 10 Shares won an outstanding +962.5% as opposed to the S&P 500’s +329.4%. Now our Director of Analysis is combing via 4,000 corporations coated through the Zacks Rank to handpick the most productive 10 tickers to shop for and cling. Don’t omit your likelihood to get in on those shares once they’re launched on January 3.

Be First To New Best 10 Shares >>

Need the newest suggestions from Zacks Funding Analysis? Nowadays, you’ll be able to obtain 7 Absolute best Shares for the Subsequent 30 Days. Click on to get this loose document

ResMed Inc. (RMD): Unfastened Inventory Research Record

To learn this newsletter on Zacks.com click on right here.

Zacks Funding Analysis