It’s been a risky begin to the yr for the most important marketplace averages, and the Nasdaq 100 Index (QQQ) has been the weaker index, sliding greater than 18% from its highs. Since its January low, the ETF has recovered just about part of its features, rallying 10% following an especially oversold studying on January twenty fourth. Paypal (PYPL) and AMD (AMD) are two most sensible tech shares that traders will have to glance to shop for at the pullback.

shutterstock.com – StockNews

shutterstock.com – StockNews

It’s been a risky begin to the yr for the most important marketplace averages, and the Nasdaq 100 Index (QQQ) has been the weaker index, sliding greater than 18% from its highs. Since its January low, the ETF has recovered just about part of its features, rallying 10% following an especially oversold studying on January twenty fourth. This has ended in a spike in bullish sentiment, with the worry and temporary panic from two weeks in the past now changed with some greed and trust that the marketplace is headed again to new highs briefly order.

Given this shift in sentiment and the sturdy oversold soar we’ve noticed, I imagine it’s much more likely that the Nasdaq-100 may just re-test its lows or even undercut its January twenty fourth low ahead of the correction is in spite of everything over. On the other hand, this can be a nice time to organize a buy-list in case the marketplace does undercut its low, for the reason that this permits one to behave if the time comes vs. scrambling to seek out concepts amid the volatility when it may be difficult to drag the cause. On this replace, we’ll have a look at two names that glance very relatively valued if we see additional weak point over the approaching weeks.

(Supply: TC2000.com)

The This fall Income Season has definitely been eventful within the tech house, with very bifurcated effects amongst other names. Complex Micro Units (AMD) is one identify that posted any other sturdy quarter of outstanding efficiency and has rallied sharply from its lows because the announcement. In the meantime, PayPal (PYPL) reported mediocre effects however ghastly steerage, reeling in its earlier expansion estimates.

In PYPL’s case, the decline under $150.00 was once justified. On the other hand, the inventory is down any other 18% since its violation of the $150.00 degree. In AMD’s case, the inventory appears too reasonable if it might proceed to submit blowout effects and is without doubt one of the few examples of expansion at a cheap value. That is evidenced via its spectacular 59% compound annual EPS expansion fee if it might meet FY2023 annual EPS estimates. Let’s take a better have a look at each corporations under and their respectively low-risk purchase issues:

Starting with PayPal, its most up-to-date quarter was once some of the worst we’ve noticed because the Tech Income Season started, with earnings coming in at ~$6.92BB, translating to simply 13% expansion year-over-year. This interprets to a 2-year reasonable gross sales expansion fee of 18%, which definitely made it tough to justify the inventory’s top class more than one. On the other hand, it was once the corporate’s steerage that was once unpalatable. That is in response to an FY2022 information with overall fee quantity anticipated to develop simply 19%, earnings anticipated to develop simplest 16%, and annual EPS projected to develop simply 2% year-over-year.

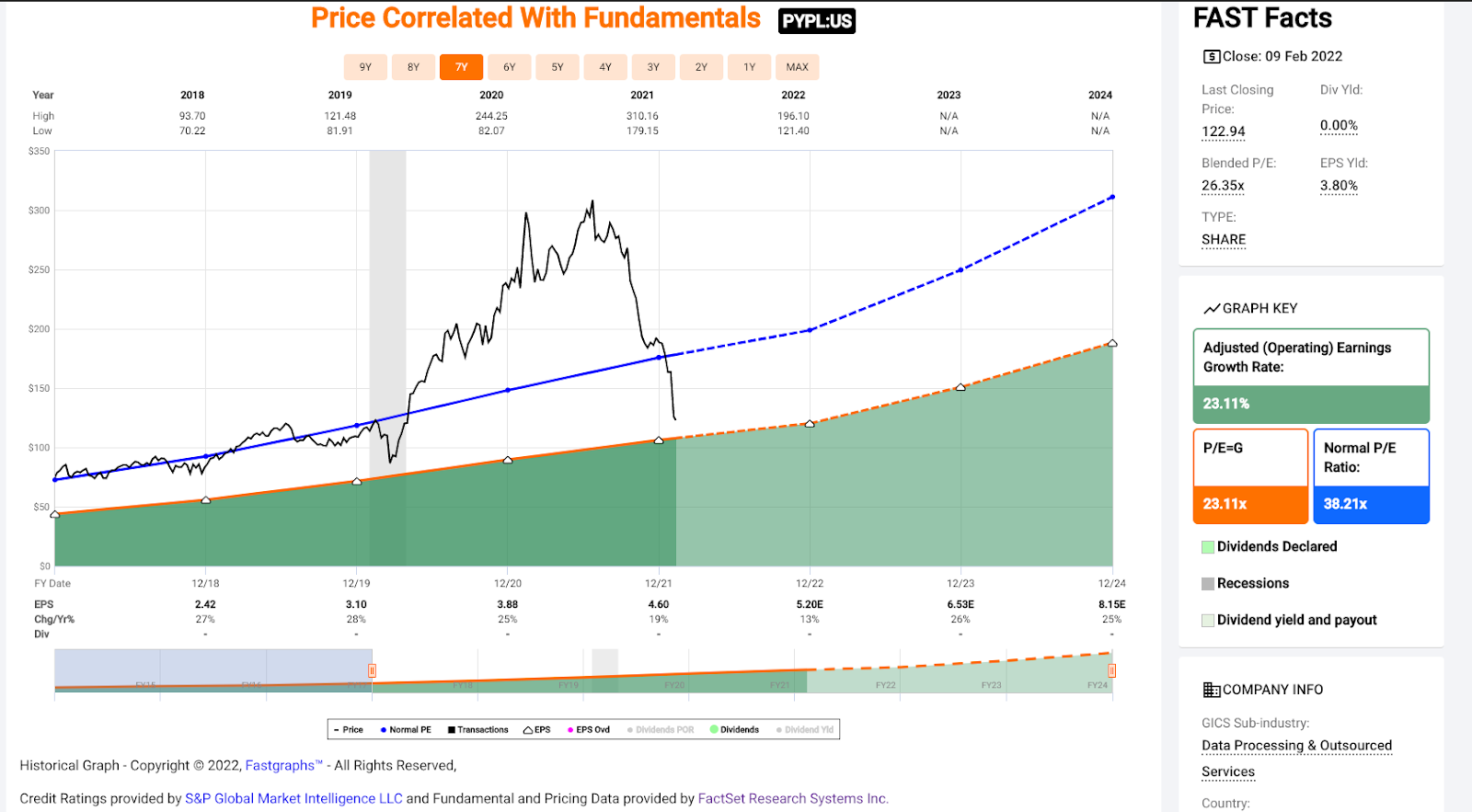

As PYPL’s ancient income development displays under, the corporate has traditionally grown annual EPS at a compound annual expansion fee of ~23.4%, which is phenomenal and has made it some of the marketplace leaders within the FinTech house. On the other hand, after plugging in FY2022 estimates of $4.69, this compound annual EPS expansion fee is anticipated to slow down via just about 350 foundation issues year-over-year. That is the very last thing that the marketplace desires to peer, particularly for a corporation that’s commanded a top class more than one. Therefore, the pointy sell-off within the inventory will have to no longer be overly sudden.

(Supply: FactSet.com, Creator’s Chart)

The excellent news is that whilst FY2022 is anticipated to be a softer yr, annual EPS is projected to bop again in FY2023, with analysts comfortable with estimates between $5.65 and $5.95, or a median estimate of $5.79. Even in the course of this vary, this may translate to a slight growth in PYPL’s long term compound annual EPS expansion fee (20.5%) and a minor sequential uptick. Clearly, the important thing shall be assembly those estimates, but when the corporate can meet or beat those estimates, a lot of the negativity appears to be priced into PYPL.

(Supply: FASTGraphs.com)

Taking a look at PayPal’s valuation above, we will be able to see that it has traditionally traded at between 38-40x income and lately trades at simply ~21.4x FY2023 income estimates at a proportion value of $124.00. Given the deceleration within the expansion fee we’ve noticed, I don’t imagine it is smart to suppose that PYPL would proceed to command a more than one very similar to its upper expansion years. Due to this fact, I imagine a extra conservative more than one is 27.

On the other hand, even beneath conservative assumptions (27 more than one and $5.70 in FY2023 annual EPS), PayPal’s truthful price is available in at $153.90. This issues to a 24% upside from present ranges and bakes in a significant margin of protection. It’s additionally value noting that when this waterfall decline, the inventory has discovered itself backtesting a big breakout degree at $121.00, and not using a significant resistance till $179.00. With the inventory having lower than $3.00 in problem to fortify and greater than $50.00 in upside to resistance, any pullbacks under $120.00 will have to be offering a fantastic access level for long-term traders.

(Supply: TC2000.com)

Transferring over to Complex Micro Units, we noticed the close to reverse, with AMD reporting blowout effects. The corporate’s This fall gross sales got here in at $4.83BB, up 49% year-over-year, which overwhelmed estimates via greater than $300MM or just about 7%. In the meantime, quarterly EPS soared to $0.92, up 77% year-over-year and 20% above estimates of $0.76. This was once helped via an exquisite quarter with upper reasonable promoting costs because of a positive product combine with Ryzen processor gross sales and powerful call for for top class desktop and pocket book PCs constructed with Ryzen 5000 processors.

In the meantime, in its Undertaking, Embedded, and Semi-Customized phase, earnings soared 75% year-over-year and 17% sequentially because of upper EPYC and semi-custom processor gross sales, whilst working source of revenue progressed because of gross sales leverage and a positive product combine. This mix of margin enlargement (50% vs. 45%) and powerful earnings expansion helped AMD develop quarterly income in keeping with proportion just about in step with ultimate quarter’s expansion (78%) and greater than 110% year-over-year ($2.79 vs. $1.29). So, whilst AMD will have appeared dear at 100x FY2020 income, it now trades at simply 47x trailing income.

(Supply: YCharts.com, Creator’s Chart)

If we have a look at AMD’s income development above, we will be able to see that whilst FY2021 was once an out of this world yr, this expansion is ready to proceed. That is in response to FY2022 and FY2023 estimates sitting at $3.96 and $4.68, respectively, forecasting 67% expansion in annual EPS over the following two years. If those estimates are met, this will likely give AMD an industry-leading compound annual EPS expansion fee of 59%, which is definitely above its ancient reasonable. According to what I imagine to be a conservative income more than one of 40, and FY2023 annual EPS estimates of $4.68, this issues to additional upside, with an excellent price nearer to $187.00.

(Supply: TC2000.com)

On the other hand, whilst AMD stays relatively valued at $132.00, the inventory has simply rallied greater than 20% off its fresh lows, and ceaselessly sharp rallies like this are retraced, particularly if the marketplace has no longer already made its cyclical low. So, I don’t see any reason why to hurry into AMD right here above $132.00, even though the corporate simply reported blowout income. As a substitute, I imagine the perfect purchase level for the inventory is at $100.00 or decrease if the inventory can re-test or undercut its fresh low and its 250-day transferring reasonable. In abstract, AMD is a smart identify to place on one’s watch-list, however I’d no longer pay up for the inventory right here.

With the Nasdaq-100 rallying greater than 10% from its fresh lows and lots of the concern from two weeks in the past having subsided, I don’t imagine that is the time to pay up for tech names. Having mentioned that, PYPL has diverged from the gang after you have decimated following a brutal This fall file, and AMD stays a marketplace chief, so any undercuts of its fresh fortify degree will have to supply a purchasing alternative. To summarize, whilst I’m really not a purchaser of PYPL and AMD at present ranges (I’m lengthy PYPL from $119.50), I’d view any pullbacks under $120.00 on PYPL and $100.00 on AMD as purchasing alternatives.

Disclosure: I’m lengthy PYPL

Disclaimer: Taylor Dart isn’t a Registered Funding Guide or Monetary Planner. This writing is for informational functions simplest. It does no longer represent an be offering to promote, a solicitation to shop for, or a advice relating to any securities transaction. The guidelines contained on this writing will have to no longer be construed as monetary or funding recommendation on any material. Taylor Dart expressly disclaims all legal responsibility in recognize to movements taken in response to any or the entire knowledge in this writing.

PYPL stocks have been buying and selling at $120.41 in keeping with proportion on Friday morning, up $1.39 (+1.17%). Yr-to-date, PYPL has declined -36.15%, as opposed to a -5.22% upward thrust within the benchmark S&P 500 index throughout the similar duration.

Concerning the Creator: Taylor Dart

Taylor has over a decade of making an investment revel in, with a distinct center of attention at the valuable metals sector. Along with running with ETFDailyNews, he’s a distinguished creator on In quest of Alpha. Be told extra about Taylor’s background, at the side of hyperlinks to his most up-to-date articles.

Extra…

The submit 2 Tech Shares to Purchase Right through the Marketplace Correction seemed first on StockNews.com